Descargar la presentación

La descarga está en progreso. Por favor, espere

1

LAS CAUSAS REALES DE LA CRISIS FINANCIERA David Saied ANALISTA ECONOMICO

2

AGENDA 1. Las Causas de la Crisis Financiera? Desregulacion o Regulacion? Desregulacion o Regulacion? 2. La verdadera Causa Raiz de la Crisis: El Ciclo Economico Austriaco – Teoria El Ciclo Economico Austriaco – Teoria 3. Problemas Estructurales (en la realidad) Ahorro y Credito

Ahorro y Credito.")

3

CAUSAS RAIZ DE LA CRISIS?

4

DESREGULACIÓN Gramm-Leach-Bliley Act of 1999 permitió la fusión entre bancos de inversión y bancos comerciales Gramm-Leach-Bliley Act of 1999 permitió la fusión entre bancos de inversión y bancos comerciales Neal-Riegle Interstate Banking Act of 1994 permite la banca a nivel nacional al eliminar las restricciones geográficas a sucursales Neal-Riegle Interstate Banking Act of 1994 permite la banca a nivel nacional al eliminar las restricciones geográficas a sucursales Depository Institutions Deregulation and Monetary Control Act of 1980, eliminó los techos en los intereses de los depósitos Depository Institutions Deregulation and Monetary Control Act of 1980, eliminó los techos en los intereses de los depósitos

5

DEREGULATION Gramm-Leach-Bliley Act of 1999 allowed commercial and investment banks to consolidate Gramm-Leach-Bliley Act of 1999 allowed commercial and investment banks to consolidate Neal-Riegle Interstate Banking Act of 1994 which established nationwide banking by removing geographic restrictions on branching Neal-Riegle Interstate Banking Act of 1994 which established nationwide banking by removing geographic restrictions on branching Depository Institutions Deregulation and Monetary Control Act of 1980, which removed ceilings on deposit interest rates Depository Institutions Deregulation and Monetary Control Act of 1980, which removed ceilings on deposit interest rates

6

REGULACION 3.1 Bank Secrecy Act 3.1 Bank Secrecy Act 3.1 Bank Secrecy Act 3.1 Bank Secrecy Act 3.2 Fair Credit Reporting Act (FCRA) 3.2 Fair Credit Reporting Act (FCRA) 3.2 Fair Credit Reporting Act (FCRA) 3.2 Fair Credit Reporting Act (FCRA) 3.3 Lending Limits 3.3 Lending Limits 3.3 Lending Limits 3.3 Lending Limits 3.4 Pass Through Insurance (PTI) 3.4 Pass Through Insurance (PTI) 3.4 Pass Through Insurance (PTI) 3.4 Pass Through Insurance (PTI) 3.5 Right to Financial Privacy Act 3.5 Right to Financial Privacy Act 3.5 Right to Financial Privacy Act 3.5 Right to Financial Privacy Act 3.6 Sarbanes-Oxley Act of 2002 3.6 Sarbanes-Oxley Act of 2002 3.6 Sarbanes-Oxley Act of 2002 3.6 Sarbanes-Oxley Act of 2002 3.7 USA PATRIOT Act 3.7 USA PATRIOT Act 3.7 USA PATRIOT Act 3.7 USA PATRIOT Act 3.8 Federal Reserve regulations 3.8 Federal Reserve regulations 3.8 Federal Reserve regulations 3.8 Federal Reserve regulations 3.8.1 Regulation A - Extensions of Credit by Federal Reserve Banks 3.8.1 Regulation A - Extensions of Credit by Federal Reserve Banks 3.8.1 Regulation A - Extensions of Credit by Federal Reserve Banks 3.8.1 Regulation A - Extensions of Credit by Federal Reserve Banks 3.8.2 Regulation B - Equal Credit Opportunity 3.8.2 Regulation B - Equal Credit Opportunity 3.8.2 Regulation B - Equal Credit Opportunity 3.8.2 Regulation B - Equal Credit Opportunity 3.8.3 Regulation C - Home Mortgage Disclosure Act (HMDA) 3.8.3 Regulation C - Home Mortgage Disclosure Act (HMDA) 3.8.3 Regulation C - Home Mortgage Disclosure Act (HMDA) 3.8.3 Regulation C - Home Mortgage Disclosure Act (HMDA) 3.8.4 Regulation D - Reserve Requirements for Depository Institutions 3.8.4 Regulation D - Reserve Requirements for Depository Institutions 3.8.4 Regulation D - Reserve Requirements for Depository Institutions 3.8.4 Regulation D - Reserve Requirements for Depository Institutions 3.8.5 Regulation E - Electronic Funds Transfer Act 3.8.5 Regulation E - Electronic Funds Transfer Act 3.8.5 Regulation E - Electronic Funds Transfer Act 3.8.5 Regulation E - Electronic Funds Transfer Act 3.8.6 Regulation F - Limitations on Interbank Liabilities 3.8.6 Regulation F - Limitations on Interbank Liabilities 3.8.6 Regulation F - Limitations on Interbank Liabilities 3.8.6 Regulation F - Limitations on Interbank Liabilities 3.8.7 Regulation O - Loans to Insiders 3.8.7 Regulation O - Loans to Insiders 3.8.7 Regulation O - Loans to Insiders 3.8.7 Regulation O - Loans to Insiders 3.8.8 Regulation P - Privacy of Consumer Financial Information 3.8.8 Regulation P - Privacy of Consumer Financial Information 3.8.8 Regulation P - Privacy of Consumer Financial Information 3.8.8 Regulation P - Privacy of Consumer Financial Information 3.8.9 Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types 3.8.9 Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types 3.8.9 Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types 3.8.9 Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types 3.8.10 Regulation W - Transactions Between Member Banks and Their Affiliates 3.8.10 Regulation W - Transactions Between Member Banks and Their Affiliates 3.8.10 Regulation W - Transactions Between Member Banks and Their Affiliates 3.8.10 Regulation W - Transactions Between Member Banks and Their Affiliates 3.8.11 Regulation Z - Truth in Lending 3.8.11 Regulation Z - Truth in Lending 3.8.11 Regulation Z - Truth in Lending 3.8.11 Regulation Z - Truth in Lending 3.8.12 Regulation AA - Unfair or Deceptive Acts or Practices 3.8.12 Regulation AA - Unfair or Deceptive Acts or Practices 3.8.12 Regulation AA - Unfair or Deceptive Acts or Practices 3.8.12 Regulation AA - Unfair or Deceptive Acts or Practices 3.8.13 Regulation BB - Community Reinvestment Act (CRA) 3.8.13 Regulation BB - Community Reinvestment Act (CRA) 3.8.13 Regulation BB - Community Reinvestment Act (CRA) 3.8.13 Regulation BB - Community Reinvestment Act (CRA) 3.8.14 Regulation CC - Expedited Funds Availability Act 3.8.14 Regulation CC - Expedited Funds Availability Act 3.8.14 Regulation CC - Expedited Funds Availability Act 3.8.14 Regulation CC - Expedited Funds Availability Act 3.8.15 Regulation DD - Truth in Savings Act 3.8.15 Regulation DD - Truth in Savings Act 3.8.15 Regulation DD - Truth in Savings Act 3.8.15 Regulation DD - Truth in Savings Act

3.2 Fair Credit Reporting Act (FCRA) 3.2 Fair Credit Reporting Act (FCRA) 3.2 Fair Credit Reporting Act (FCRA) 3.3 Lending Limits 3.3 Lending Limits 3.3 Lending Limits 3.3 Lending Limits 3.4 Pass Through Insurance (PTI) 3.4 Pass Through Insurance (PTI) 3.4 Pass Through Insurance (PTI) 3.4 Pass Through Insurance (PTI) 3.5 Right to Financial Privacy Act 3.5 Right to Financial Privacy Act 3.5 Right to Financial Privacy Act 3.5 Right to Financial Privacy Act 3.6 Sarbanes-Oxley Act of Sarbanes-Oxley Act of Sarbanes-Oxley Act of Sarbanes-Oxley Act of USA PATRIOT Act 3.7 USA PATRIOT Act 3.7 USA PATRIOT Act 3.7 USA PATRIOT Act 3.8 Federal Reserve regulations 3.8 Federal Reserve regulations 3.8 Federal Reserve regulations 3.8 Federal Reserve regulations Regulation A - Extensions of Credit by Federal Reserve Banks Regulation A - Extensions of Credit by Federal Reserve Banks Regulation A - Extensions of Credit by Federal Reserve Banks Regulation A - Extensions of Credit by Federal Reserve Banks Regulation B - Equal Credit Opportunity Regulation B - Equal Credit Opportunity Regulation B - Equal Credit Opportunity Regulation B - Equal Credit Opportunity Regulation C - Home Mortgage Disclosure Act (HMDA) Regulation C - Home Mortgage Disclosure Act (HMDA) Regulation C - Home Mortgage Disclosure Act (HMDA) Regulation C - Home Mortgage Disclosure Act (HMDA) Regulation D - Reserve Requirements for Depository Institutions Regulation D - Reserve Requirements for Depository Institutions Regulation D - Reserve Requirements for Depository Institutions Regulation D - Reserve Requirements for Depository Institutions Regulation E - Electronic Funds Transfer Act Regulation E - Electronic Funds Transfer Act Regulation E - Electronic Funds Transfer Act Regulation E - Electronic Funds Transfer Act Regulation F - Limitations on Interbank Liabilities Regulation F - Limitations on Interbank Liabilities Regulation F - Limitations on Interbank Liabilities Regulation F - Limitations on Interbank Liabilities Regulation O - Loans to Insiders Regulation O - Loans to Insiders Regulation O - Loans to Insiders Regulation O - Loans to Insiders Regulation P - Privacy of Consumer Financial Information Regulation P - Privacy of Consumer Financial Information Regulation P - Privacy of Consumer Financial Information Regulation P - Privacy of Consumer Financial Information Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types Regulation Q - Prohibition Against Payment of Interest on Certain Deposit Account Types Regulation W - Transactions Between Member Banks and Their Affiliates Regulation W - Transactions Between Member Banks and Their Affiliates Regulation W - Transactions Between Member Banks and Their Affiliates Regulation W - Transactions Between Member Banks and Their Affiliates Regulation Z - Truth in Lending Regulation Z - Truth in Lending Regulation Z - Truth in Lending Regulation Z - Truth in Lending Regulation AA - Unfair or Deceptive Acts or Practices Regulation AA - Unfair or Deceptive Acts or Practices Regulation AA - Unfair or Deceptive Acts or Practices Regulation AA - Unfair or Deceptive Acts or Practices Regulation BB - Community Reinvestment Act (CRA) Regulation BB - Community Reinvestment Act (CRA) Regulation BB - Community Reinvestment Act (CRA) Regulation BB - Community Reinvestment Act (CRA) Regulation CC - Expedited Funds Availability Act Regulation CC - Expedited Funds Availability Act Regulation CC - Expedited Funds Availability Act Regulation CC - Expedited Funds Availability Act Regulation DD - Truth in Savings Act Regulation DD - Truth in Savings Act Regulation DD - Truth in Savings Act Regulation DD - Truth in Savings Act")

7

REGULACION Community Reinvestment Act of 1977, ley que fomenta operación y créditos en comunidades, incluyendo barrios de bajos ingresos Community Reinvestment Act of 1977, ley que fomenta operación y créditos en comunidades, incluyendo barrios de bajos ingresos EQUAL CREDIT OPPORTUNITY ACT 1976 & 1993, promover préstamos a minorías y prohibe la discriminación por sexo, raza, color, religión, estado civil o edad EQUAL CREDIT OPPORTUNITY ACT 1976 & 1993, promover préstamos a minorías y prohibe la discriminación por sexo, raza, color, religión, estado civil o edad

8

REGULATION Community Reinvestment Act of 1977, a law enacted to meet the credit needs of their entire communities, including low- and moderate-income neighborhoods Community Reinvestment Act of 1977, a law enacted to meet the credit needs of their entire communities, including low- and moderate-income neighborhoods EQUAL CREDIT OPPORTUNITY ACT 1976 & 1993, to promote the availability of credit to all creditworthy applicants without regard to race, color, religion, national origin, sex, marital status, or age EQUAL CREDIT OPPORTUNITY ACT 1976 & 1993, to promote the availability of credit to all creditworthy applicants without regard to race, color, religion, national origin, sex, marital status, or age

9

Publicacion de la Reserva Federal- Equal Opp Act- Sobrerregulacion? El no cumplir con la Ley de Igualdad de Oportunidad…puede someter al banco a pasivos civiles y daños punitivos…[que] pueden llegar a $10,000 en caso individual y hasta $500,000 mil en acción de clases…

10

Failure to comply with the Equal Credit Opportunity Act or Regulation B can subject a financial institution to civil liability for actual and punitive damages. Liability for punitive damages can be as much as $10,000 in individual actions and the lesser of $500,000…

11

Publicacion de la Reserva cont. (sobre estandares para hipotecas) 1. Ausencia de historial de crédito no debe ser visto como un factor negativo…(!) 2. Participación en programas educativos de crédito es otra forma en que los aplicantes pueden demostrar su habilidad de manejar sus deudas responsablemente… 3. … [bancos] pueden permitir que regalos, donaciones o préstamos por parte de familiares [u otras fuentes] se acepten como abono inicial…(!) 4. [Se] aceptarán como ingresos válidos los siguientes: trabajo estacional, subsidios de beneficiencia (welfare) y beneficios de desempleo…(!!)

2. Participación en programas educativos de crédito es otra forma en que los aplicantes pueden demostrar su habilidad de manejar sus deudas responsablemente… 3. … [bancos] pueden permitir que regalos, donaciones o préstamos por parte de familiares [u otras fuentes] se acepten como abono inicial…(!) 4. [Se] aceptarán como ingresos válidos los siguientes: trabajo estacional, subsidios de beneficiencia (welfare) y beneficios de desempleo…(!!).")

12

Publicacion de la Reserva (sobre estandares cont.) 5. …aunque no se deben considerar niveles no razonables de deuda, debemos notar que el mercado secundario esta dispuesto a considerar razones de hipoteca por encima del estándar de 28/36… La Reserva Federal sugiere que la razón de 28/36 (participacion de ingreso a pagos hipotecarios) que se ha usado históricamente no debe aplicar para individuos pobres aún y cuando los registros indican que estos tienen menores ahorros y que tienen mayor, no menor, probabilidad de tener problemas manejando mayores niveles de deuda. Stan Leibowitz

que se ha usado históricamente no debe aplicar para individuos pobres aún y cuando los registros indican que estos tienen menores ahorros y que tienen mayor, no menor, probabilidad de tener problemas manejando mayores niveles de deuda. Stan Leibowitz.")

13

Lack of credit history should not be seen as a negative factor Lack of credit history should not be seen as a negative factor Participation in credit counseling or …education programs is another way that applicants can demonstrate an ability to manage their debts responsibly. Participation in credit counseling or …education programs is another way that applicants can demonstrate an ability to manage their debts responsibly. Lenders may wish to allow gifts, grants, or loans from relatives, (and others)… Lenders may wish to allow gifts, grants, or loans from relatives, (and others)… Fannie Mae/Freddie Mac will accept the following as valid income sources:...seasonal work, …welfare payments, and unemployment benefits(!) Fannie Mae/Freddie Mac will accept the following as valid income sources:...seasonal work, …welfare payments, and unemployment benefits(!)

… Lenders may wish to allow gifts, grants, or loans from relatives, (and others)… Fannie Mae/Freddie Mac will accept the following as valid income sources:...seasonal work, …welfare payments, and unemployment benefits(!) Fannie Mae/Freddie Mac will accept the following as valid income sources:...seasonal work, …welfare payments, and unemployment benefits(!).")

14

La Causa Raiz de la Crisis Teoría: El Ciclo Económico Austriaco

15

Oferta y Demanda de Fondos Equilibrio y Mayor Ahorro Ahorro, Inversión, Crédito O D inin O=I=Cr in = Tasa natural o de mercado Tasa de Interés de Mercado O i' n

16

Mercado de Fondos: Expansión Artificial del Crédito (Dislocamiento) (Dislocamiento) Ahorro, Inversión, Crédito O D inin I im = Tasa implicita I a = Tasa artificial baja O+ M I=Cr i im iaia S Tasa **

(Dislocamiento) Ahorro, Inversión, Crédito O D inin I im = Tasa implicita I a = Tasa artificial baja O+ M I=Cr i im iaia S Tasa **")

17

Tasas Bajas Distorsionan en Favor de Proyectos de Largo Plazo TIPO DE PROYECTO2%4%6%8% REPAGO EN CORTO PLAZO$6,994.70$4,344.45$2,003.43($67.50) REPAGO EN LARGO PLAZO$11,009.32$3,758.54($2,101.25)($6,844.02)

REPAGO EN LARGO PLAZO$11,009.32$3,758.54($2,101.25)($6,844.02)")

18

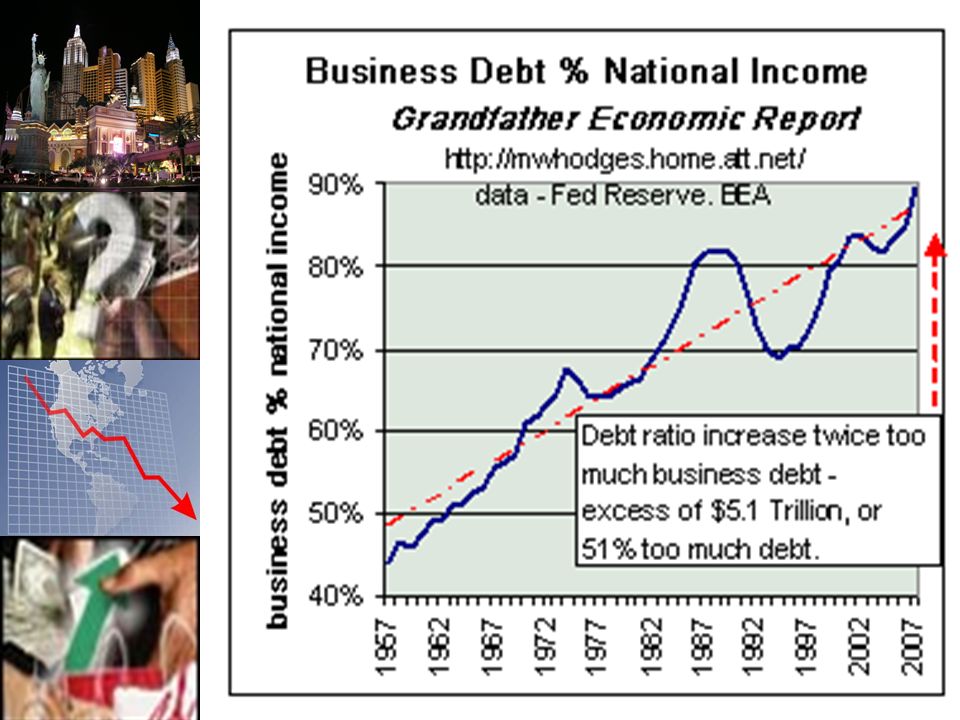

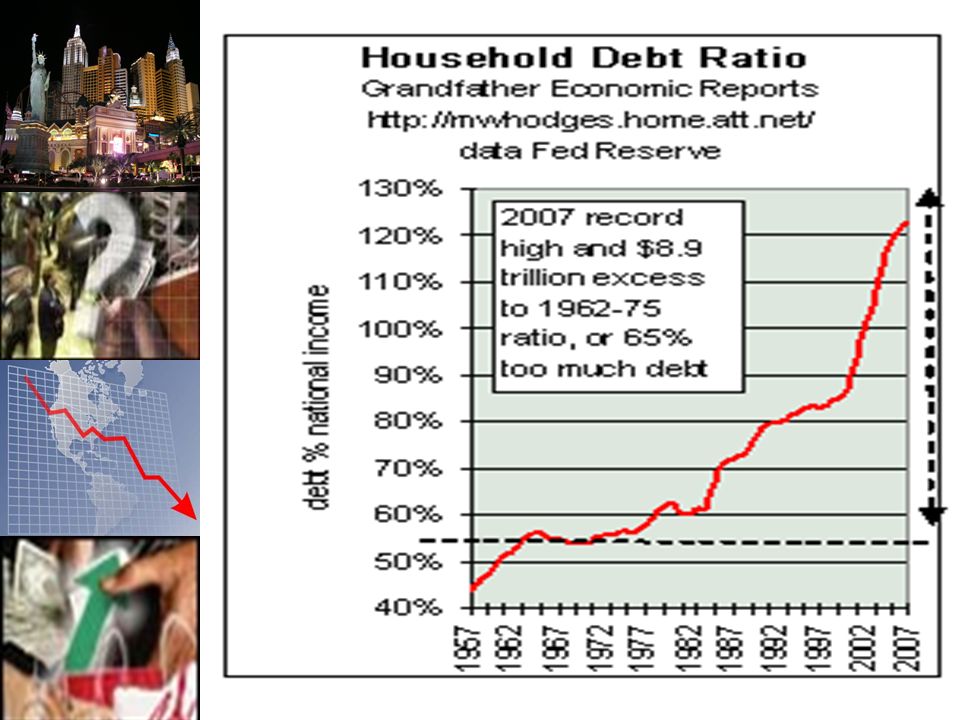

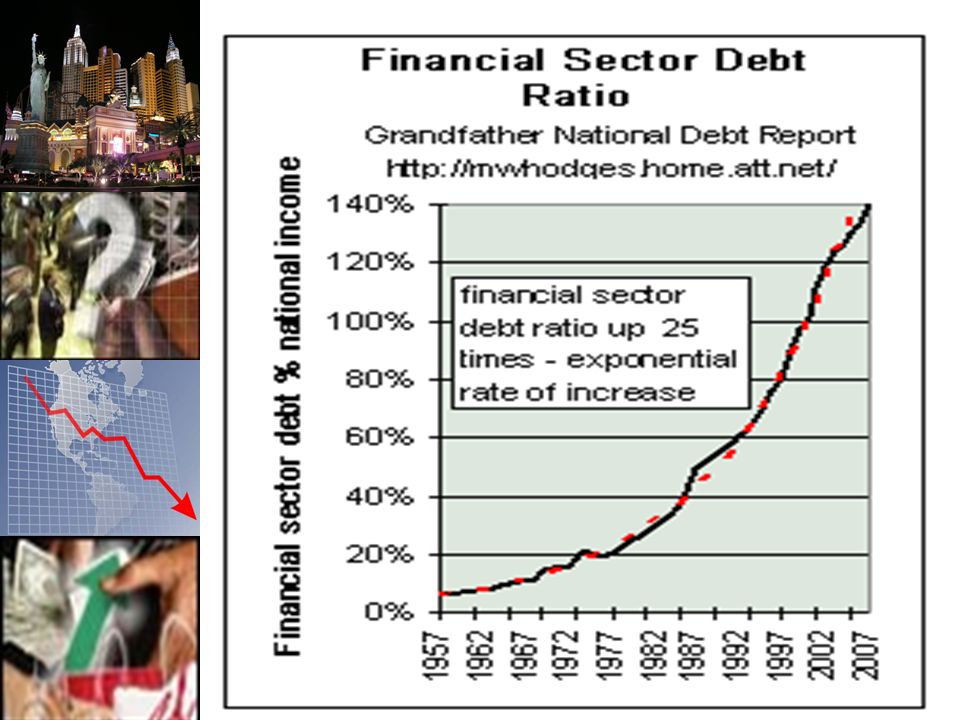

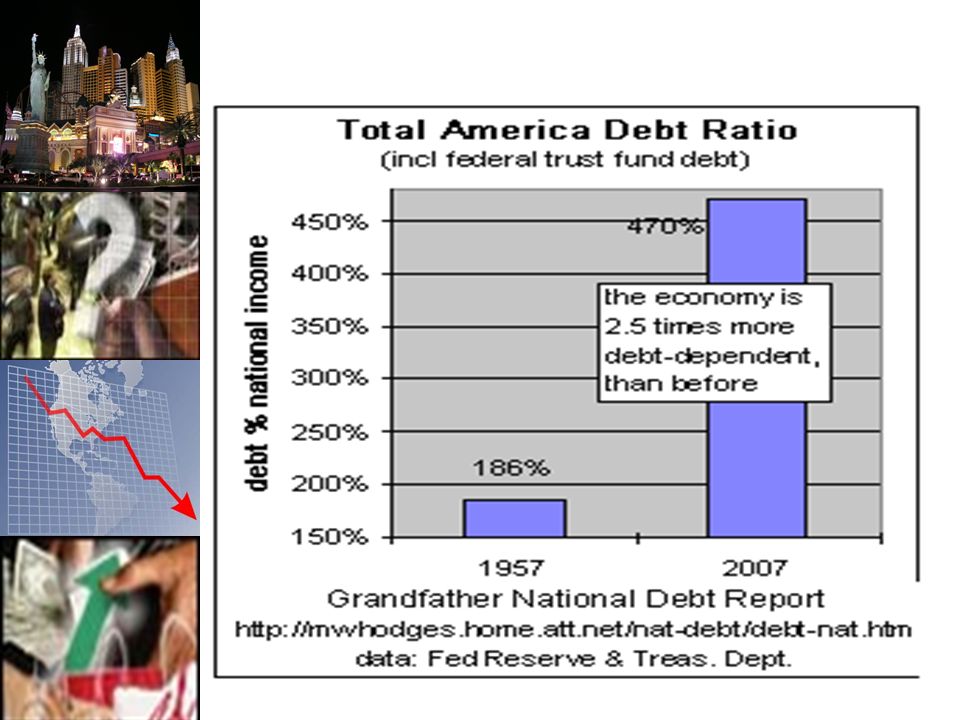

La Causa Raiz de la Crisis La Realidad: Dislocación entre ahorro y crédito

19

Long Term Short Term Rates Source: Federal Reserve

20

El Mercado estaba funcionando…

21

Hasta que la Reserva Intervino

22

World Savings Rate as % of GDP (source: Table A16, IMF) 1986- 1993 1994 - 2001 200220032004200520062007 22.722.120.520.821.922.523.323.7 Excedentes de Ahorro de Mercados Emergentes?

Excedentes de Ahorro de Mercados Emergentes")

23

Tasas Reales en Negativo

24

CAUSA RAIZ DE CRISIS: TASAS BANCA EN NEGATIVO (~5 AÑOS!!)

")

25

Unemploym 1948-08 Source: BLS

26

Bajas Tasas Fomentan Desahorro

27

Necesitamos más crédito? Ben Bernanke Oct/20/08 Ben Bernanke asked Congress for a second stimulus package to increase credit availability to consumers, homebuyers and businesses. To stimulate lending: Congress might consider guarantees or partial guarantees, it might consider direct lending…

32

Greenspan sobre las bajas tasas de interés (Ago 2005) La historia no ha manejado de manera noble con los efectos posteriores a periodos prolongados de bajas tasas de riesgo

La historia no ha manejado de manera noble con los efectos posteriores a periodos prolongados de bajas tasas de riesgo")

33

Source: Federal Reserve Credit Crisis Begins Aug 2007

34

Alan Greenspan 1967 [En las recesiones] los banqueros rápidamente se percatan de que sus préstamos son excesivos con respecto a sus reservas…y empiezan a reducir sus nuevos créditos, cobrando tasas de interés mas altas. Esto obliga a los prestamistas a mejorar su rentabilidad antes de que puedan obtener más crédito… Por consiguiente, …un sistema de banca libre se erige como el protector de la establidad y el crecimiento económico…

![Alan Greenspan 1967 [En las recesiones] los banqueros rápidamente se percatan de que sus préstamos son excesivos con respecto a sus reservas…y empiezan a reducir sus nuevos créditos, cobrando tasas de interés mas altas.](http://images.slideplayer.es/3/1074249/slides/slide_34.jpg "Esto obliga a los prestamistas a mejorar su rentabilidad antes de que puedan obtener más crédito… Por consiguiente, …un sistema de banca libre se erige como el protector de la establidad y el crecimiento económico….")

35

Greenspan on Low Interest Rates (Aug 2005) History has not dealt kindly with the aftermath of protracted periods of low risk premiums.

History has not dealt kindly with the aftermath of protracted periods of low risk premiums.")

36

MUCHAS GRACIAS!

37

Banks want to raise rates

38

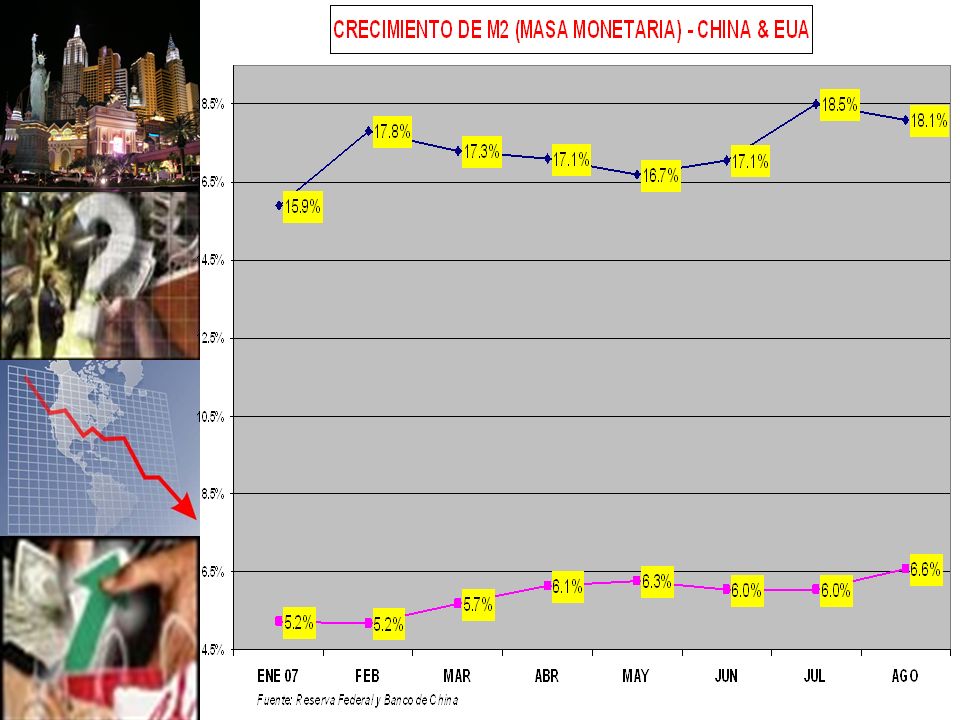

ECB EXPANDE M2 EN EUROPA

41

Average 4.4%

Presentaciones similares

European Transfer Credit System (ECTS) Methodology in.>")

. It features two verb changes that we will see very soon.>")