Descargar la presentación

La descarga está en progreso. Por favor, espere

1

UE consumidor –hoy y ayer Some stastistics : figures can lie and liars can figure

2

La letra menuda Any conclusions drawn from -or actions taken based on- this presentation or its hard and soft copies and the dissemination thereof during social events are solely for the responsibility of the reader or viewer and are not supported nor confirmed by the author, nor Mr. Hans Klunder, nor the Government of the Netherlands neither of any of the other member or associated states of the European Union.

3

Finland Sweden Denmark England Ireland Netherlands Belgium Germany France Spain Italy Poland Baltic States Hungria Bulgaria Romania Greece 0 1 2 3 4 5 La UNIÓN Europea……………………..? TOBACCO ALCOHOL PORCENTAGE DE INGRESO

4

WOOPIES DINKIES YUPPIES 5% 20% 7% 15% 6% 10% PORCENTAGE POPULACIÓN PORCENTAGE DEL CONSUMO Segmentos del mercado UE

5

20 – 25 years 25 – 35 years 35 – 45 years 45 – 55 years 55 – 65 years Over 65 years 0102030405060 Emancipación………………………….. MUJERES CON SUELDO MAYOR A LOS HOMBRES

6

Shop untill you drop…………………. SHOPS INTERNET MAIL ORDER TELESALES HOME VISITS 0 25 50 75 100 CANALES DE DISTRIBUCIÓN

7

Qué nos muestra esta gráfica ? CHAIN STORES INDEPENDENT STORES DEPARTMENT STORES OTHER OUTLETS MAIL ORDER HYPERS SUPERS 40 30 20 10 0

8

Conclusión ………………………? I BUY DESIGNER BRANDS MANY PEOPLE I KNOW BUY DESIGNER BRANDS DESIGNER BRANDS ARE OVER PRICED DESIGNER BRANDS ARE HIGHER QUALITY EUROPE 21 42 75 22 LATIN AMERICA 24 67 82 39 USA/CANADA 14 41 87 18 ASIA-PACIFIC 20 39 79 35 OTHERS 21 44 77 28

9

Botar ó reparar ……………….? 2001 2003 2005 2007 105 100 95 90 85 GARMENTS OTHER CLOTHING CLEANING AND REPAIR 29, 00 9, 00

10

En quién confiamos ……………….? TELEVISION RADIO MAGAZINE NEWSPAPER CINEMA SEARCH ENG BRAND WEBSITES RECOMMENDATION ON LINE OPINION EMAILS 0 25 50 75 100 CONFIANZA EN FUENTES

11

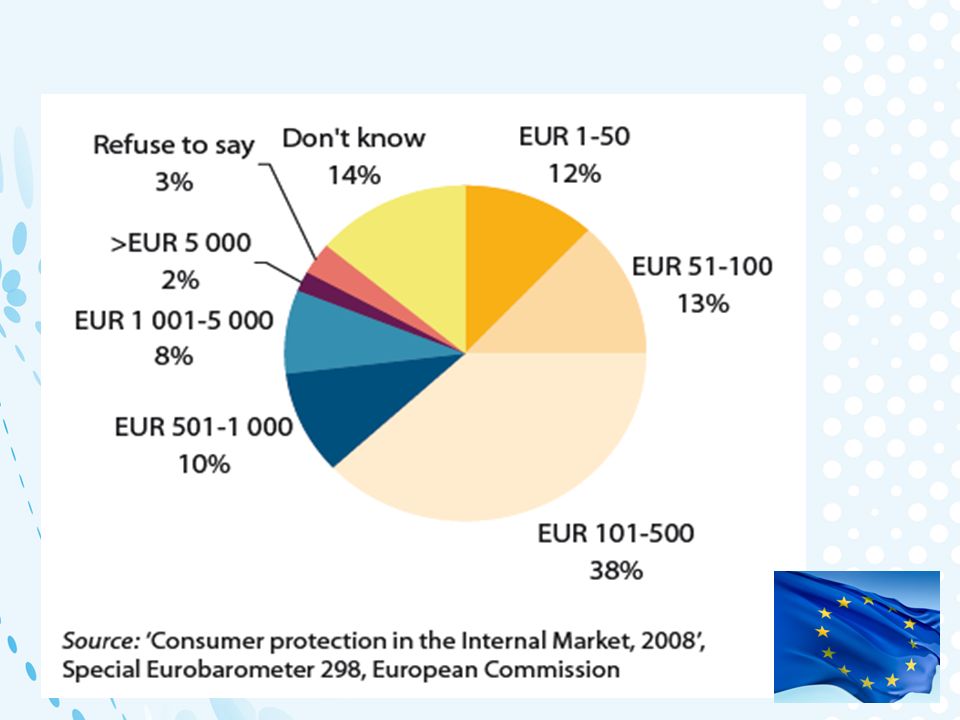

Sleepless in Valletta………………. Stockholm Copenhague Berlin London Amsterdam Brussels Paris Madrid Roma Valletta Ankara Vienna Prague 0 10 20 30 40 50 60 % PERSONAS PREOCUPADOS POR LOS PAGOS DE FIN DE MES

12

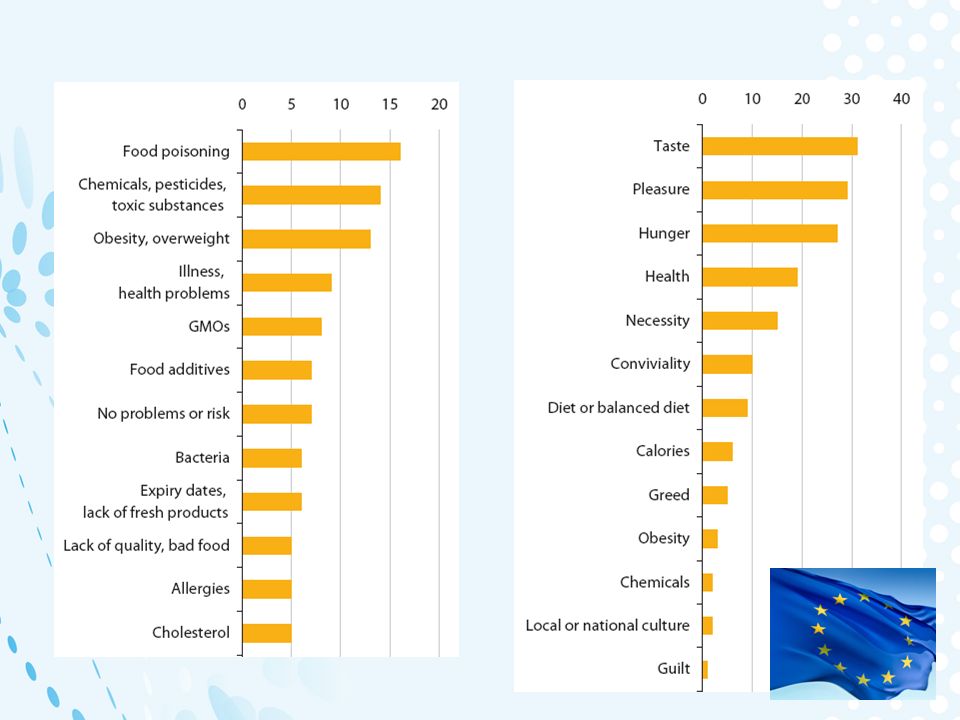

Yo compro solamente comida fresca..! CALIDAD (?) SABOR PRECIO DISPONIBLE MARCA FRESCURA SALUD SEGURIDAD PROCESO ORIGEN 0 10 20 30 40 PURCHASING FACTORS FOR FOOD

SABOR PRECIO DISPONIBLE MARCA FRESCURA SALUD SEGURIDAD PROCESO ORIGEN PURCHASING FACTORS FOR FOOD.")

13

Investigación por Universidad de Wageningen: on purchasing factors en alimentos 96%: Sabor, salud, precio 4%: Salud de animales ambiente, negocio justo, producto casera Los temas de interes bajo se considera como responsabilidad del gobierno, proveedores y otros Consumidores no saben diferenciar las etiquetas en caldiad de alimentos

14

Dónde compramos la comida………..? 1 2 3 % FinlandKESKOSOKTRADEKA80 SwedenKAAXFOODKF91 DenmarkCOOPDANSKSUPERGROS86 EnglandTESCOSAINSBURYASDA58 NetherlandsAHOLDLAURUSTSM59 BelgiumCARREFOURDELHAIZECOLRUYT68 GermanyEDEKAREWEALDI55 FranceCARREFOURLECLERCINTERMARCHE64 SpainCARREFOURMERCADONAEROSKI54 ItalyCOOPCONADCARREFOUR27 PortugalSONAEJMRINTERMARCHE47

15

Productores contra supermercados PROLIFERATION OF PRIVATE LABELS

16

1,09 1,49 1,69

18

http://ec.europa.eu/consumers_ europe_edition2_en.pdf or www.cbi.eu or h.verhulst@cbi.eu

19

MAASTRICHT BRUSSELS ANTWERP BRUGHES AMSTERDAM THE HAGUE BELGIUM GERMANY POLLOS96.000.000 PERSONAS16.500.000 BICICLETAS16.000.000 CERDOS12.000.000 CARROS10.000.000 VACAS4.000.000 PERROS1.500.000 OBEJAS1.000.000 DEBAJO MAR26% LECHE/VACA32 ltr MAS BAJO-11 mtr MAS ALTO+ 323 mtr MIN- 18 o C MAX+ 35 o C GDP± 300 bln IMP/EXP± 300 bln NATIONA…171 ALTURA (H)1.83 m ROTTERDAM

1.83 m ROTTERDAM")

20

AT Austria BE Belgium BG Bulgaria CZ Czech Republic DK Denmark DE Germany EE Estonia IE Ireland EL Greece ES Spain FR France IT Italy CY Cyprus LV Latvia LT Lithuania LU Luxembourg HU Hungary MT Malta NL Netherlands PL Poland PT Portugal RO Romania SI Slovenia SK Slovakia FI Finland SE Sweden UK United Kingdom HR Croatia TR Turkey IS Iceland LI Liechtenstein NO Norway CH Switzerland Consolidated total of realised added values in a country Sum of all primary incomes Sum of all spendings by households, enterprises and government in the country

21

TABACO ALCOHOL

24

PREMIUM PRIVATE LABEL BRANDS Maximizing the profit margin of a product- category by entering the luxury segment Offering high price niche products within the PL assortment Drugstores Selected Hypermarkets ME-TOO Improving profits by opening the price- entrance class Discounter Replacing challenger brands by copies of market leaders GENERIC Reaction against Me-too pr. by traditional retail Supermarkets Addition of price-entrance class beside traditional brands UMBRELLA- BRAND One PL brand-name for a whole category (s) Strengthening the retailer image Whole Retail RETAILER STRATEGY PL TYPES CORPORATE BRAND Branding Private Labels Selected Retailers Confidence transfer of retailer brand attributes on their products GLOBAL/ REGIONAL BRANDS Internation al Retailers Developing strong PL products to compete with regional/ global brands Expanding a brand through the European countries

Strengthening the retailer image Whole Retail RETAILER STRATEGY PL TYPES CORPORATE BRAND Branding Private Labels Selected Retailers Confidence transfer of retailer brand attributes on their products GLOBAL/ REGIONAL BRANDS Internation al Retailers Developing strong PL products to compete with regional/ global brands Expanding a brand through the European countries.")

Presentaciones similares

Conversation between Ana & Miguel based on the conversation and select the phrase that tells what Miguel wants or.>")

Noviembre de 2004.>")

To revise colours 2) to learn 12 countries 3) To play toca 4) To play brain gym 5) To say which countries you woud like to / wouldnt like to.>")